Lending (Supply USDC)

Lending on PredMart is the process of depositing USDC into the protocol's lending pool to earn yield. When you supply USDC, you are providing liquidity that borrowers can use to take loans against their Polymarket shares. In return, you receive a share of the interest payments that borrowers pay on their outstanding loans.

This page explains every aspect of the lending process — how deposits work, what pUSDC vault shares are, how yield accrues, how to withdraw, and what risks lenders face.

How Lending Works

PredMart's lending pool is built on the ERC-4626 tokenized vault standard — an Ethereum standard specifically designed for yield-bearing vaults. This standard defines a common interface that makes PredMart's vault shares composable with other DeFi protocols and tooling.

When you deposit USDC into the pool, the smart contract mints pUSDC (PredMart USDC) vault shares to your wallet. These shares represent your proportional ownership of the total pool. As borrowers pay interest, the total pool value grows, and the value of each pUSDC share increases accordingly.

The Core Mechanism

Here's how the lending pool operates at a fundamental level:

- Lenders deposit USDC → The pool's

totalAssetsincreases, and pUSDC shares are minted to the lender. - Borrowers take loans → USDC leaves the pool's available balance but remains counted in

totalAssets(as outstanding debt). - Interest accrues → The

totalBorrowAssetsgrows continuously as borrowers owe more over time. This increasestotalAssets. - Lenders withdraw → pUSDC shares are burned, and the lender receives their proportional share of the pool — which is now larger due to accrued interest.

The key insight is that totalAssets = available USDC in the pool + total outstanding debt. As interest accrues on the debt, totalAssets grows, making each pUSDC share worth more USDC than when it was minted.

Depositing USDC

Step-by-Step Process

- Navigate to the Lending page on predmart.com/lending

- Approve USDC spending (first time only): If you haven't previously approved the lending pool contract to spend your USDC, you'll be prompted to do so. This is a standard ERC-20 approval transaction.

- Enter the deposit amount: Specify how much USDC you want to deposit into the pool.

- Confirm the transaction: Review the details in your wallet and confirm. The transaction will:

- Transfer your USDC from your wallet to the lending pool contract

- Mint pUSDC vault shares to your wallet

- Receive pUSDC shares: Once the transaction is confirmed on-chain, you'll see your pUSDC balance in your wallet and on the PredMart interface.

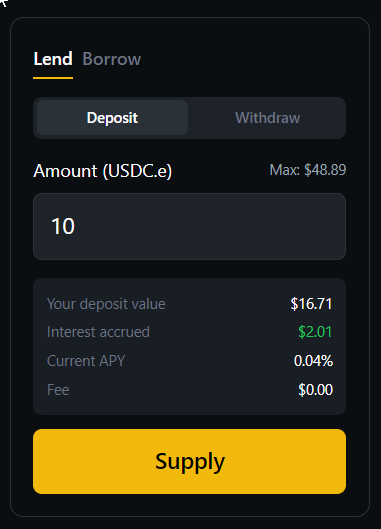

Below is the deposit interface. In this example, the user is supplying 10 USDC. The panel shows the current deposit value ($16.71), interest already accrued ($2.01), and the current APY (0.04%). No fees are charged for depositing.

How Many pUSDC Shares Do I Receive?

The number of pUSDC shares you receive depends on the current exchange rate between USDC and pUSDC. This rate is determined by the following formula:

shares = deposit_amount × total_pUSDC_supply / total_pool_assets

When the pool is first created, the exchange rate starts at 1:1 (with a decimal offset). Over time, as interest accrues, the exchange rate shifts — each pUSDC share becomes worth more USDC.

Example:

- The pool currently holds 100,000 USDC in total assets

- There are 95,000 pUSDC shares outstanding

- The exchange rate is: 1 pUSDC = 100,000 / 95,000 = 1.0526 USDC

- If you deposit 10,000 USDC, you receive: 10,000 / 1.0526 = 9,500 pUSDC shares

- Your 9,500 pUSDC shares are immediately worth 10,000 USDC — but over time, they'll be worth more as interest continues to accrue

Decimal Offset

PredMart's vault uses a decimal offset of 6 for pUSDC shares. While USDC has 6 decimals, pUSDC has 12 decimals (6 + 6). This offset is a standard practice in ERC-4626 vaults to prevent a class of rounding attacks known as "inflation attacks." It does not affect the value of your deposit — it's purely a precision enhancement at the smart contract level.

Understanding pUSDC Vault Shares

What Are pUSDC Shares?

pUSDC is an ERC-20 token that represents your ownership of the PredMart lending pool. It is not a stablecoin — its value relative to USDC changes over time. Specifically, 1 pUSDC is designed to always be worth at least 1 USDC, and its value grows as borrowers pay interest.

Think of pUSDC like a share of a mutual fund. The fund (lending pool) holds a portfolio of assets (USDC + outstanding loans). As the portfolio generates returns (interest income), the share price (pUSDC-to-USDC exchange rate) increases.

Key Properties of pUSDC

| Property | Details |

|---|---|

| Token Standard | ERC-20 |

| Decimals | 12 |

| Transferable | Yes — you can send pUSDC to any wallet |

| Yield-Bearing | Yes — value increases over time as interest accrues |

| Redeemable | Yes — can be burned to withdraw USDC from the pool |

| Composable | Yes — compatible with any DeFi protocol that accepts ERC-20 tokens |

pUSDC Value Over Time

The value of 1 pUSDC in terms of USDC follows this trajectory:

- At pool launch: 1 pUSDC ≈ 1 USDC (with decimal offset adjustment)

- Over time: 1 pUSDC > 1 USDC, growing continuously as interest accrues

- The rate never decreases under normal conditions — it only goes up as borrowers pay interest

The only scenario where pUSDC value could decrease is if bad debt occurs — when a borrower's debt exceeds their collateral value and the shortfall is socialized across all lenders. This is discussed in detail in the Risks for Lenders section below.

How Yield Accrues

Interest Income

All yield in PredMart's lending pool comes from borrower interest payments. When a borrower takes a USDC loan, they pay interest at a rate determined by the protocol's interest rate model. This interest accrues continuously (calculated per-second) and is added to the pool's total assets.

Supply APY

The Supply APY (Annual Percentage Yield) that lenders earn is directly derived from the borrow rate and the pool's utilization:

Supply APY = Borrow APR × Utilization Rate × (1 - Reserve Factor)

Where:

- Borrow APR is the annual interest rate borrowers pay (see Interest Rates)

- Utilization Rate is the percentage of the pool that is currently lent out (total borrowed / total assets)

- Reserve Factor is the protocol fee — currently 5% (0.05). This portion of interest income goes to PredMart's protocol reserves rather than to lenders.

Example:

- Borrow APR = 15%

- Utilization = 60%

- Reserve Factor = 5%

- Supply APY = 15% × 60% × (1 - 5%) = 15% × 0.60 × 0.95 = 8.55%

Why Supply APY is Lower Than Borrow APR

The supply APY is always lower than the borrow APR for two reasons:

-

Utilization dilution: Not all USDC in the pool is borrowed. Idle USDC earns no interest. If only 60% of the pool is borrowed, the interest income is "diluted" across 100% of the supplied USDC.

-

Reserve factor: 5% of all interest income goes to protocol reserves, not to lenders.

Real-Time Accrual

Interest in PredMart accrues continuously — not daily, not hourly, but every second. Technically, the contract calculates interest at the per-second level each time a state-changing function is called (borrow, repay, deposit, withdraw, etc.). Between interactions, interest is "virtual" — it's owed but hasn't been formally recorded. The moment anyone interacts with the contract, all pending interest is settled and reflected in the pool's state.

This means:

- Your pUSDC value is always up-to-date (the contract calculates the latest exchange rate on every call)

- There's no "interest payment date" — yield is continuous

- You start earning interest the moment your deposit transaction is confirmed

Withdrawing USDC

How to Withdraw

- Navigate to the Lending page

- Switch to the Withdraw tab

- Enter the amount of USDC you wish to withdraw

- Confirm the transaction in your wallet

- The contract will burn your pUSDC shares and transfer the corresponding USDC to your wallet

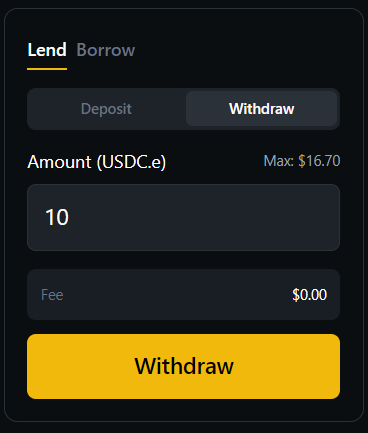

Below is the withdrawal interface. The user is withdrawing 10 USDC from their lending position. The maximum available balance is shown at the top right.

Withdraw vs. Redeem

The ERC-4626 standard provides two ways to exit:

- Withdraw: Specify the amount of USDC you want to receive. The contract calculates and burns the appropriate number of pUSDC shares.

- Redeem: Specify the number of pUSDC shares you want to burn. The contract calculates and sends you the corresponding USDC amount.

Both achieve the same result — you're exchanging pUSDC for USDC. The difference is just which side of the equation you specify.

Available Liquidity

You can only withdraw USDC that is currently available in the pool. Available liquidity is:

Available Liquidity = Total Pool USDC Balance - (not the borrowed portion)

Or more precisely: it's the USDC that is sitting in the contract, not currently lent out to borrowers.

If the pool has high utilization (most USDC is lent out), there may not be enough available liquidity for large withdrawals. In this scenario:

- You can withdraw up to the available balance

- As borrowers repay their loans, more liquidity becomes available

- The high utilization rate will drive up interest rates (via the kinked rate model), incentivizing borrowers to repay sooner and new lenders to deposit — both of which increase available liquidity

In extreme scenarios (near 100% utilization), withdrawals may be temporarily limited. This is an inherent feature of lending pool designs — your USDC is being productively used by borrowers. The interest rate model's steep slope above 80% utilization is specifically designed to prevent this situation and rapidly restore available liquidity when it occurs.

Monitoring Your Position

Pool Statistics

The Lending page displays real-time pool statistics:

| Metric | Description |

|---|---|

| Total Supplied | Total USDC deposited by all lenders |

| Total Borrowed | Total USDC currently lent out to borrowers |

| Available Liquidity | USDC available for new borrows or withdrawals |

| Utilization Rate | Percentage of the pool that is borrowed (total borrowed / total supplied) |

| Supply APY | Current annualized yield for lenders |

| Borrow APR | Current annualized interest rate for borrowers |

Your Position

Your individual lending position shows:

| Metric | Description |

|---|---|

| pUSDC Balance | Number of pUSDC shares you hold |

| USDC Value | Current value of your pUSDC in USDC terms |

| Yield Earned | Total interest income earned since your deposit |

Rate History Charts

PredMart records pool statistics every 30 seconds and provides historical rate charts with three time windows:

- 1 Week: Shows the most recent week of supply APY and utilization data

- 1 Month: Provides a broader view of rate trends

- 6 Months: Shows long-term rate patterns

These charts help you understand rate trends and make informed decisions about when to deposit or withdraw.

Risks for Lenders

Lending on PredMart carries certain risks that you should understand before depositing:

Bad Debt Risk

Bad debt occurs when a borrower's position becomes "underwater" — meaning the value of their collateral falls below their outstanding debt. When this happens during liquidation, the debt that cannot be recovered is socialized across all lenders in the pool.

In practical terms, bad debt reduces totalAssets without a corresponding reduction in pUSDC supply, which decreases the exchange rate. All lenders share the loss proportionally to their pool ownership.

PredMart mitigates bad debt risk through several mechanisms:

- Conservative LTV ratios: The 7-anchor LTV curve ensures that borrowers cannot take on excessive leverage relative to their collateral value.

- Liquidation buffer: The liquidation threshold is set 10% above the LTV ratio, providing a cushion before bad debt occurs.

- Real-time liquidation: The WebSocket-based liquidation engine responds within seconds of a price drop, minimizing the window for positions to go underwater.

- Depth-gated borrow caps: Limits borrowing against illiquid tokens to amounts that can be efficiently liquidated.

Utilization Risk (Temporary Illiquidity)

If pool utilization is very high, you may not be able to withdraw all your USDC immediately. Your funds are not lost — they are lent to borrowers — but you may need to wait for borrowers to repay or for utilization to decrease.

The kinked interest rate model is specifically designed to address this: once utilization exceeds 80% (the "kink"), interest rates increase dramatically (up to 300% APR at 100% utilization), creating strong economic incentives for borrowers to repay and for new lenders to deposit.

Smart Contract Risk

As with any DeFi protocol, there is a risk that a bug or vulnerability in PredMart's smart contract could lead to loss of funds. PredMart mitigates this through careful development practices, but users should be aware that no smart contract system is completely risk-free.

Market-Wide Risk

In a scenario where multiple Polymarket markets resolve unfavorably for borrowers simultaneously, the pool could experience significant bad debt. While the probability of this is low (due to the diversity of markets and positions), it represents a tail risk for lenders.

FAQ for Lenders

Q: Is there a minimum deposit amount? A: There is no protocol-enforced minimum deposit. However, extremely small deposits may not be economical due to gas fees (though Polygon gas fees are very low).

Q: Can I deposit and withdraw at any time? A: Yes, you can deposit at any time. Withdrawals are available up to the pool's available liquidity. There is no lock-up period.

Q: Do I need to claim my interest? A: No. Interest accrues automatically in the value of your pUSDC shares. When you withdraw, you receive your original deposit plus all accrued interest.

Q: What happens if utilization is 100%? A: You cannot withdraw until some liquidity is returned to the pool (via borrower repayments or new deposits). The extreme interest rate at high utilization (up to 300% APR) strongly incentivizes rapid normalization.

Q: Can I lose money as a lender? A: Yes, in theory, if bad debt exceeds the accrued interest on your position. However, the protocol's risk parameters are designed to make this extremely unlikely under normal market conditions.

Next Steps

- Interest Rates — Understand the interest rate model that determines your yield

- Borrowing — Learn how the other side of the pool works

- Risk Parameters — Deep dive into the risk management system

- Liquidation — Understand how liquidation protects lenders